oto car insurance used car repair

oto car insurance used car repair

Car Insurance Premium: Understanding Affects Your Rates . Car insurance premiums can seem like a mystery, but understanding what affects your rates can help you make informed decisions and potentially save money. In this article, we’ll explore the factors that influence car insurance premiums, offer tips to reduce your rates, and answer some frequently asked questions about car insurance.

What is a Car Insurance Premium?

A car insurance premium is the amount of money you pay for your car insurance policy. This payment can be made monthly, quarterly, semi-annually, or annually, depending on the terms set by your insurance provider. The premium is determined based on various factors, including your personal information, driving history, and the type of coverage you choose.

Factors Influencing Car Insurance Premiums

- Driving Record: Your driving history is one of the most significant factors affecting your premium. Accidents, traffic violations, and claims can increase your rates.

- Age and Gender: Younger drivers, especially teenagers, and male drivers typically face higher premiums due to higher risk factors.

- Location: Where you live impacts your premium. Urban areas with higher traffic and crime rates usually result in higher premiums.

- Vehicle Type: The make, model, and age of your vehicle play a role in determining your premium. Expensive and high-performance cars cost more to insure.

- Coverage Level: The more coverage you have, the higher your premium will be. Comprehensive and collision coverage adds to the cost.

- Credit Score: In some regions, insurance companies use credit scores to assess risk, with lower scores often leading to higher premiums.

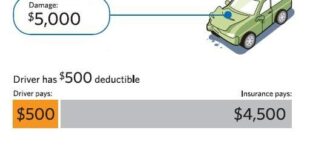

- Deductible Amount: A higher deductible can lower your premium, but it means you’ll pay more out-of-pocket if you file a claim.

- Mileage: The more you drive, the higher the risk of accidents, leading to higher premiums for high-mileage drivers.

- Marital Status: Married individuals often receive lower premiums compared to single drivers.

- Claims History: A history of multiple claims can signal higher risk, increasing your premium.

How to Lower Your Car Insurance Premium

- Maintain a Clean Driving Record: Avoid accidents and traffic violations to keep your premium low.

- Shop Around: Compare quotes from different insurance companies to find the best rate.

- Bundle Policies: Combine your car insurance with other policies, like home insurance, for discounts.

- Increase Your Deductible: Opt for a higher deductible to lower your premium, but ensure you can afford it in case of a claim.

- Take Advantage of Discounts: Ask about discounts for good driving, low mileage, safety features, and more.

- Improve Your Credit Score: Better credit scores can lead to lower premiums.

- Choose the Right Vehicle: Consider insurance costs when buying a car; some vehicles are cheaper to insure.

- Limit Coverage on Older Vehicles: Drop comprehensive and collision coverage on older cars to save money.

- Pay Annually: Paying your premium in full annually can sometimes result in a discount.

- Complete a Defensive Driving Course: Many insurers offer discounts for completing approved driving courses.

10 Tips to Reduce Your Car Insurance Premium

- Regularly Review Your Policy: Make sure your coverage is up-to-date and fits your current needs.

- Consider Usage-Based Insurance: Programs that track your driving habits can offer lower rates for safe driving.

- Install Safety Devices: Anti-theft devices and safety features can lower your risk and your premium.

- Limit Teen Drivers: Adding a teen driver can significantly increase your premium; consider restricting their usage.

- Work with an Independent Agent: Agents can help you find the best rates and policies tailored to your needs.

- Maintain a Good Driving Record: Avoid speeding tickets and other violations to keep your record clean.

- Check for Low Mileage Discounts: If you drive less than average, you might qualify for a low-mileage discount.

- Avoid Small Claims: Paying for minor repairs out-of-pocket can prevent your premium from increasing.

- Stay Loyal: Some insurers offer loyalty discounts for long-term customers.

- Ask for a Review: Periodically ask your insurer to review your policy for any new discounts or savings.

10 FAQs about Car Insurance Premiums

- What is a car insurance premium?

- A car insurance premium is the amount you pay for your insurance policy, which can be billed monthly, quarterly, semi-annually, or annually.

- How is my car insurance premium calculated?

- Premiums are calculated based on factors such as your driving record, age, location, vehicle type, coverage level, and credit score.

- Can I negotiate my car insurance premium?

- While you can’t negotiate the premium directly, you can shop around for better rates and take advantage of available discounts.

- Why did my car insurance premium increase?

- Premiums can increase due to factors like claims history, changes in driving record, increased coverage, or adjustments by the insurance company.

- How can I lower my car insurance premium?

- Maintain a clean driving record, bundle policies, increase your deductible, and take advantage of discounts to lower your premium.

- Is it worth increasing my deductible to lower my premium?

- It can be, but ensure you can afford the higher out-of-pocket cost if you need to file a claim.

- Does my credit score affect my car insurance premium?

- In some regions, insurance companies use credit scores to assess risk, with lower scores often leading to higher premiums.

- Do all insurance companies use the same factors to determine premiums?

- While many factors are common, each insurance company has its own formula and weightings for calculating premiums.

- Can I get a discount for being a good driver?

- Yes, many insurers offer discounts for maintaining a clean driving record or completing defensive driving courses.

- How often should I review my car insurance policy?

- It’s a good idea to review your policy annually or whenever you experience significant life changes, such as moving or buying a new car.

Conclusion

Understanding your car insurance premium and the factors that influence it can help you make informed decisions and potentially save money. By maintaining a clean driving record, shopping around for the best rates, and taking advantage of discounts, you can lower your premium and ensure you have the coverage you need. Remember to review your policy regularly and stay informed about changes in the insurance market to keep your rates as low as possible. With the right approach, managing your car insurance premium doesn’t have to be a daunting task. Instead, it can be an opportunity to optimize your coverage and enjoy peace of mind on the road.