oto car insurance used car repair

oto car insurance used car repair

Car Insurance by State: A Comprehensive Guide. Understanding car insurance by state can be a complex process due to the varying laws, regulations, and requirements across the United States. This guide aims to provide a clear and detailed overview of car insurance in different states, helping you navigate through the essential information you need to make informed decisions about your car insurance policy.

Introduction to Car Insurance by State

Car insurance is mandatory in almost every state in the U.S., but the specifics of coverage requirements and regulations can differ significantly. Understanding these differences is crucial for ensuring that you have adequate protection and are compliant with state laws. This article will cover the fundamental aspects of car insurance, highlight key differences between states, and offer practical tips for choosing the right policy for your needs.

Understanding Car Insurance Basics

1. What is Car Insurance? Car insurance is a contract between you and an insurance company that provides financial protection against physical damage or bodily injury resulting from traffic collisions and against liability that could also arise from incidents in a vehicle.

2. Types of Car Insurance Coverage

- Liability Coverage: Covers injuries and damages you cause to others.

- Collision Coverage: Pays for damage to your car from an accident.

- Comprehensive Coverage: Covers non-collision-related damage.

- Personal Injury Protection (PIP): Covers medical expenses for you and your passengers.

- Uninsured/Underinsured Motorist Coverage: Protects you if the at-fault driver doesn’t have adequate insurance.

State-Specific Car Insurance Requirements

Each state has its own requirements for car insurance. Here is a detailed look at some key states:

1. California

- Minimum Liability Coverage: 15/30/5 (Bodily injury per person/accident, Property damage)

- Optional Coverages: Collision, Comprehensive, Uninsured Motorist

2. Texas

- Minimum Liability Coverage: 30/60/25

- Additional Options: Personal Injury Protection, Collision, Comprehensive

3. New York

- Minimum Liability Coverage: 25/50/10

- No-Fault Insurance: Requires PIP coverage

4. Florida

- Minimum Liability Coverage: 10/20/10

- No-Fault State: PIP is mandatory

5. Illinois

- Minimum Liability Coverage: 25/50/20

- Uninsured Motorist Coverage: Required

How to Choose the Right Car Insurance Policy

1. Assess Your Needs Consider factors such as the value of your car, your driving habits, and your financial situation.

2. Compare Quotes Get quotes from multiple insurers to compare coverage options and prices.

3. Understand the Terms Read the policy terms carefully to understand what is and isn’t covered.

4. Check for Discounts Look for discounts for safe driving, bundling policies, or having safety features in your car.

Factors Affecting Car Insurance Rates

1. Driving Record A clean driving record typically results in lower premiums.

2. Age and Gender Young drivers and males often face higher rates due to higher risk factors.

3. Location Insurance rates can vary based on where you live due to factors like crime rates and traffic density.

4. Credit Score Many insurers use credit scores to help determine rates.

5. Vehicle Type The make, model, and age of your car can affect insurance costs.

State-by-State Comparison

1. Highest Average Premiums

- Michigan: Known for its high premiums due to comprehensive coverage requirements.

- Louisiana: High rates due to frequent claims and severe weather.

2. Lowest Average Premiums

- Vermont: Low rates due to fewer accidents and less traffic.

- Maine: Known for its low crime rate and low number of claims.

Tips for Lowering Your Car Insurance Premiums

- Maintain a Clean Driving Record Avoid accidents and traffic violations to keep premiums low.

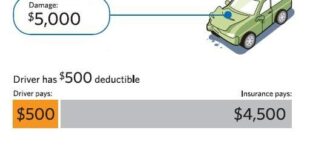

- Increase Your Deductible Higher deductibles can lower your premium but mean higher out-of-pocket costs in an accident.

- Bundle Policies Combine car insurance with other policies like homeowners or renters insurance for discounts.

- Take Advantage of Discounts Ask about discounts for safety features, good grades (for students), or completing defensive driving courses.

- Review Your Coverage Regularly Adjust your coverage as your needs change to avoid overpaying.

10 Tips for Managing Car Insurance by State

- Research State Requirements Understand the minimum coverage required in your state.

- Shop Around Compare quotes from different insurers.

- Ask About Discounts Check for available discounts to lower your premium.

- Bundle Policies Consider bundling car insurance with other policies.

- Maintain Good Credit A good credit score can help lower your rates.

- Opt for Higher Deductibles If you can afford it, higher deductibles can reduce your premium.

- Drive Safely Avoid accidents and violations to keep your insurance costs low.

- Install Safety Features Cars with safety features often qualify for discounts.

- Consider Usage-Based Insurance Pay-as-you-drive policies can be cost-effective for infrequent drivers.

- Review Your Policy Annually Make sure your coverage still meets your needs.

10 Frequently Asked Questions About Car Insurance by State

1. What is the minimum car insurance required in my state? Minimum requirements vary by state and typically include liability coverage.

2. Can I drive without insurance in any state? No, almost all states require car insurance to legally drive.

3. What happens if I drive without insurance? Penalties can include fines, license suspension, and even jail time.

4. How can I find the cheapest car insurance? Compare quotes from different insurers and look for discounts.

5. What is no-fault insurance? In no-fault states, your insurance covers your own injuries regardless of who is at fault.

6. Can my credit score affect my insurance rates? Yes, many insurers use credit scores to help determine premiums.

7. Are there states with particularly high insurance rates? Yes, states like Michigan and Louisiana have high average premiums.

8. Can I switch car insurance companies at any time? Yes, you can switch insurers, but check for any cancellation fees.

9. What should I do if I can’t afford car insurance? Look for state assistance programs or minimum coverage options.

10. How do I know if I’m getting enough coverage? Assess your personal needs and risks, and consult with an insurance agent.

Conclusion

Navigating car insurance by state can seem daunting due to the variations in requirements and regulations. However, by understanding the basics of car insurance, assessing your needs, and comparing policies, you can find the right coverage for your situation. Always remember to review your policy regularly and stay informed about state-specific requirements to ensure you’re adequately protected. Properly managing your car insurance not only keeps you compliant with state laws but also provides peace of mind on the road.