oto car insurance used car repair

oto car insurance used car repair

Car Insurance Coverage: Everything You Need to Know. Car insurance coverage is an essential aspect of vehicle ownership that provides financial protection against various risks and uncertainties. Understanding the types of coverage available, their benefits, and how to choose the right policy can help you make informed decisions and ensure you are adequately protected. This comprehensive guide will explore the intricacies of car insurance coverage, including tips and frequently asked questions to help you navigate the process.

Types of Car Insurance Coverage

1. Liability Coverage

Liability coverage is mandatory in most states and covers bodily injury and property damage that you may cause to others in an accident. It consists of two components:

- Bodily Injury Liability (BIL): Pays for medical expenses, lost wages, and legal fees if you injure someone in an accident.

- Property Damage Liability (PDL): Covers the cost of repairing or replacing another person’s property damaged in an accident you caused.

2. Collision Coverage

Collision coverage pays for the repair or replacement of your vehicle if it is damaged in a collision with another car or object, regardless of who is at fault. This coverage is particularly important for newer or more valuable vehicles.

3. Comprehensive Coverage

Comprehensive coverage protects against non-collision-related damages, such as theft, vandalism, natural disasters, and hitting an animal. It ensures that your vehicle is covered for a wide range of potential risks.

4. Personal Injury Protection (PIP)

Personal Injury Protection, also known as no-fault insurance, covers medical expenses, lost wages, and other related costs for you and your passengers, regardless of who is at fault in an accident. PIP is mandatory in some states.

5. Uninsured/Underinsured Motorist Coverage

This coverage provides protection if you are involved in an accident with a driver who has no insurance or insufficient insurance to cover the damages. It helps pay for medical expenses, lost wages, and other costs.

6. Medical Payments Coverage

Medical payments coverage, also known as MedPay, covers medical expenses for you and your passengers regardless of fault. It can be used in conjunction with health insurance to cover deductibles and co-pays.

7. Gap Insurance

Gap insurance is crucial for those who have financed or leased their vehicle. It covers the difference between the car’s actual cash value and the amount still owed on the loan or lease if the car is totaled or stolen.

8. Towing and Labor Coverage

This optional coverage pays for towing and labor costs if your car breaks down or is involved in an accident. It provides peace of mind knowing that you have help available in an emergency.

9. Rental Reimbursement Coverage

Rental reimbursement coverage pays for a rental car if your vehicle is being repaired after an accident. This coverage ensures that you have transportation while your car is out of commission.

10. Custom Parts and Equipment Coverage

If you have added custom parts or equipment to your vehicle, this coverage ensures that they are protected in case of damage or theft. It covers items like custom wheels, sound systems, and other aftermarket modifications.

Factors Affecting Car Insurance Coverage

1. Driving Record

Your driving record plays a significant role in determining your insurance premiums. A clean driving record with no accidents or violations will generally result in lower rates.

2. Vehicle Type

The make, model, and year of your vehicle can impact your insurance costs. Expensive or high-performance cars typically have higher premiums due to the increased cost of repairs and replacement parts.

3. Location

Where you live affects your insurance rates. Urban areas with higher traffic density and crime rates usually have higher premiums than rural areas.

4. Age and Gender

Young drivers and male drivers often pay higher premiums due to statistical data showing a higher likelihood of accidents among these groups.

5. Credit Score

Many insurers use credit scores to assess risk. A higher credit score can result in lower premiums, as it indicates a lower risk of filing claims.

6. Coverage Limits and Deductibles

Choosing higher coverage limits and lower deductibles will increase your premiums but provide more comprehensive protection in case of an accident.

7. Claims History

A history of frequent claims can result in higher premiums, as insurers may view you as a higher risk.

How to Choose the Right Car Insurance Coverage

1. Assess Your Needs

Consider factors such as your vehicle’s value, your driving habits, and your financial situation when choosing coverage. Ensure that you have adequate protection without overpaying for unnecessary coverage.

2. Compare Quotes

Shop around and compare quotes from multiple insurers to find the best rates and coverage options. Use online comparison tools to streamline the process.

3. Review Policy Details

Read the fine print of each policy to understand what is covered and what is excluded. Pay attention to coverage limits, deductibles, and any additional benefits or discounts.

4. Consider Bundling

Many insurers offer discounts if you bundle your car insurance with other types of insurance, such as home or renters insurance.

5. Check for Discounts

Look for available discounts that can lower your premiums, such as safe driver discounts, multi-car discounts, and good student discounts.

6. Evaluate Customer Service

Research the customer service reputation of insurers. Read reviews and check ratings from organizations like J.D. Power and the Better Business Bureau.

Tips for Lowering Car Insurance Costs

- Maintain a Clean Driving Record: Avoid accidents and traffic violations to qualify for lower premiums.

- Take a Defensive Driving Course: Completing a defensive driving course can earn you a discount with some insurers.

- Increase Your Deductible: Raising your deductible can lower your premium, but ensure you can afford the higher out-of-pocket cost if you need to file a claim.

- Bundle Your Policies: Bundle your car insurance with other types of insurance to receive a multi-policy discount.

- Drive a Safe Car: Choose a vehicle with safety features and a good safety rating to lower your insurance costs.

- Limit Your Mileage: Low-mileage drivers may qualify for discounts, as less time on the road reduces the risk of accidents.

- Review Your Coverage Annually: Regularly review your policy to ensure you have the right coverage and are taking advantage of available discounts.

- Improve Your Credit Score: A higher credit score can result in lower insurance premiums.

- Install Anti-Theft Devices: Equipping your car with anti-theft devices can qualify you for discounts.

- Ask About Discounts: Inquire about any additional discounts you may be eligible for, such as loyalty discounts or occupational discounts.

FAQs About Car Insurance Coverage

1. What is the minimum car insurance coverage required by law?

The minimum coverage varies by state but generally includes liability coverage for bodily injury and property damage.

2. What does full coverage car insurance include?

Full coverage typically includes liability, collision, and comprehensive coverage, providing broad protection for various risks.

3. Can I drive without car insurance?

Driving without insurance is illegal in most states and can result in fines, license suspension, and other penalties.

4. How can I lower my car insurance premium?

You can lower your premium by maintaining a clean driving record, increasing your deductible, bundling policies, and taking advantage of discounts.

5. What factors affect my car insurance premium?

Factors include your driving record, vehicle type, location, age, gender, credit score, coverage limits, and claims history.

6. Is it worth having comprehensive and collision coverage on an older car?

It depends on the car’s value and your financial situation. If the cost of coverage exceeds the car’s value, it may not be worth it.

7. Can I change my car insurance coverage at any time?

Yes, you can adjust your coverage at any time, but it is best to review and make changes at your policy renewal period to avoid penalties.

8. What should I do if I’m involved in an accident?

Report the accident to your insurer immediately, exchange information with the other driver, and document the scene with photos and notes.

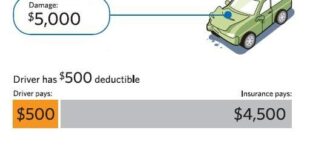

9. How does a deductible work in car insurance?

A deductible is the amount you pay out of pocket before your insurance covers the rest. Higher deductibles can lower your premiums.

10. Can I get car insurance with a bad driving record?

Yes, but you may pay higher premiums. Some insurers specialize in high-risk drivers and offer coverage options for those with poor driving records.

Conclusion

Car insurance coverage is a crucial aspect of responsible vehicle ownership, providing financial protection against a variety of risks and uncertainties. By understanding the different types of coverage available and considering factors such as your driving record, vehicle type, and personal needs, you can select the right policy to ensure you are adequately protected.

Additionally, taking steps to lower your premiums, such as maintaining a clean driving record and bundling policies, can help you save money while still receiving comprehensive coverage. Regularly reviewing your policy and staying informed about your options will help you make the best decisions for your car insurance needs.