oto car insurance used car repair

oto car insurance used car repair

Car Insurance Policy: A Guide to Understanding and Choosing the Right Coverage. Car insurance is an essential aspect of vehicle ownership that offers financial protection and peace of mind. With various policies and coverage options available, understanding the ins and outs of car insurance is crucial for making an informed decision. This guide will delve into the different types of car insurance policies, factors affecting premiums, tips for choosing the right policy, and common FAQs to help you navigate the world of car insurance.

Types of Car Insurance Policies

1. Liability Insurance

Liability insurance covers damages and injuries you cause to others in an accident. It includes:

- Bodily Injury Liability: Covers medical expenses and lost wages for the other party.

- Property Damage Liability: Covers the cost of repairing or replacing the other party’s property.

2. Collision Insurance

Collision insurance pays for repairs to your vehicle after a collision with another vehicle or object, regardless of who is at fault.

3. Comprehensive Insurance

Comprehensive insurance covers non-collision-related damages, such as theft, vandalism, natural disasters, and animal collisions.

4. Personal Injury Protection (PIP)

PIP covers medical expenses and, in some cases, lost wages for you and your passengers, regardless of who is at fault.

5. Uninsured/Underinsured Motorist Coverage

This type of insurance protects you if you’re involved in an accident with a driver who has inadequate or no insurance.

6. Medical Payments Coverage (MedPay)

MedPay covers medical expenses for you and your passengers, regardless of who is at fault, similar to PIP but typically with fewer benefits.

7. Gap Insurance

Gap insurance covers the difference between what you owe on your car loan and the car’s actual cash value if your vehicle is totaled.

8. Rental Reimbursement Coverage

This coverage helps pay for a rental car while your vehicle is being repaired after a covered loss.

9. Roadside Assistance

Roadside assistance offers support for issues like flat tires, dead batteries, and towing.

10. Custom Equipment Coverage

Covers aftermarket parts and accessories added to your vehicle, such as custom rims or audio systems.

Factors Affecting Car Insurance Premiums

1. Driving Record

A clean driving record typically results in lower premiums, while a history of accidents or traffic violations can increase your rates.

2. Vehicle Type

The make, model, and year of your vehicle affect premiums. High-performance or luxury cars often come with higher insurance costs.

3. Age and Gender

Younger drivers, especially males, may face higher premiums due to statistically higher accident rates.

4. Location

Your location can impact your insurance rates. Urban areas with higher traffic density often result in higher premiums compared to rural areas.

5. Credit Score

A higher credit score can lead to lower premiums, as insurance companies often use credit scores to assess risk.

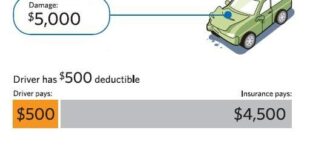

6. Deductible Amount

Choosing a higher deductible can lower your premium but means you’ll pay more out-of-pocket if you make a claim.

7. Coverage Limits

Higher coverage limits generally result in higher premiums. Adjusting your coverage to fit your needs can help manage costs.

8. Vehicle Safety Features

Cars equipped with safety features like anti-lock brakes, airbags, and anti-theft systems may qualify for discounts.

9. Driving Habits

How much and how you drive can impact your insurance rates. Frequent long-distance driving or driving in high-risk areas may increase premiums.

10. Insurance History

Having a history of continuous insurance coverage can positively affect your rates. Lapses in coverage might lead to higher premiums.

Tips for Choosing the Right Car Insurance Policy

- Assess Your Needs: Determine the level of coverage that suits your driving habits and financial situation.

- Compare Quotes: Get quotes from multiple insurers to find the best rate for the coverage you need.

- Check Discounts: Inquire about available discounts for safe driving, vehicle safety features, and bundling policies.

- Understand Coverage Options: Familiarize yourself with different types of coverage and choose what fits your needs.

- Review Policy Terms: Carefully read policy documents to understand what is covered and what is excluded.

- Evaluate Deductibles: Choose a deductible that balances your premium cost with your ability to pay out-of-pocket.

- Consider the Insurer’s Reputation: Research the insurer’s customer service and claims handling reputation.

- Adjust Coverage as Needed: Update your policy if your circumstances change, such as moving or buying a new car.

- Seek Professional Advice: Consult an insurance agent or broker for personalized guidance and recommendations.

- Regularly Review Your Policy: Periodically review and adjust your policy to ensure it continues to meet your needs.

Frequently Asked Questions (FAQs)

- What is the minimum car insurance coverage required?

- The minimum coverage varies by state but generally includes liability insurance. Check your state’s requirements for specific details.

- How can I lower my car insurance premium?

- Increase your deductible, take advantage of discounts, and maintain a clean driving record to lower your premium.

- What does collision insurance cover?

- Collision insurance covers damage to your vehicle from collisions with other vehicles or objects.

- Is comprehensive insurance worth it?

- Comprehensive insurance is valuable if you want coverage for non-collision-related incidents like theft or natural disasters.

- What is the difference between PIP and MedPay?

- PIP covers medical expenses and lost wages, while MedPay covers medical expenses only.

- What should I do if I have an accident with an uninsured driver?

- Uninsured/underinsured motorist coverage can help cover damages if you’re in an accident with an uninsured driver.

- Can I cancel my car insurance policy at any time?

- Yes, you can cancel your policy, but check with your insurer about any cancellation fees or requirements.

- How does my credit score affect my car insurance rates?

- A higher credit score can lead to lower rates, as insurers use credit scores to assess risk.

- What is gap insurance?

- Gap insurance covers the difference between the amount you owe on your car loan and the car’s actual cash value if your vehicle is totaled.

- How often should I review my car insurance policy?

- It’s a good idea to review your policy annually or when significant life changes occur.

Conclusion

Choosing the right car insurance policy is essential for protecting yourself financially and ensuring peace of mind while driving. By understanding the different types of coverage and factors that affect premiums, you can make an informed decision that suits your needs and budget. Remember to regularly review and adjust your policy as your circumstances change to maintain optimal coverage.

In summary, car insurance is not just a legal requirement but a vital aspect of responsible vehicle ownership. Taking the time to research, compare options, and select the right coverage can save you money and provide the protection you need in case of an accident or unexpected event. Make sure to stay informed and proactive to keep your car insurance in line with your evolving needs.