oto car insurance used car repair

oto car insurance used car repair

Car Insurance Requirements: What You Need to Know. Car insurance is a crucial aspect of vehicle ownership, providing financial protection in case of accidents, theft, or damage. Understanding the requirements for car insurance is essential for compliance with legal regulations and ensuring adequate coverage. This article will delve into the essential car insurance requirements, including mandatory coverage types, state-specific regulations, and tips for choosing the right policy.

1. Types of Car Insurance Coverage

Car insurance can be divided into several types of coverage, each serving a different purpose. Here are the primary types:

- Liability Insurance: Covers damages to others if you’re at fault in an accident. It includes bodily injury liability and property damage liability.

- Collision Coverage: Pays for repairs to your own vehicle after a collision, regardless of fault.

- Comprehensive Coverage: Protects against non-collision-related incidents such as theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: Provides coverage if you’re involved in an accident with a driver who lacks sufficient insurance.

- Medical Payments Coverage: Covers medical expenses for you and your passengers, regardless of fault.

2. Minimum Coverage Requirements by State

Each state in the U.S. has its own minimum car insurance requirements. It’s important to be familiar with the regulations in your state to ensure compliance:

- California: Requires liability insurance with minimum coverage of $15,000 for bodily injury per person, $30,000 per accident, and $5,000 for property damage.

- Texas: Mandates liability insurance with minimum coverage of $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage.

- New York: Requires liability insurance with minimum coverage of $25,000 for bodily injury per person, $50,000 per accident, and $10,000 for property damage.

3. Factors Affecting Insurance Premiums

Several factors can influence your car insurance premiums:

- Driving Record: A clean driving record typically results in lower premiums, while accidents and traffic violations can increase costs.

- Vehicle Type: The make, model, and age of your vehicle can impact insurance rates. High-performance or luxury vehicles often come with higher premiums.

- Location: Your geographical location affects your insurance rate. Areas with higher crime rates or accident frequencies may result in higher premiums.

- Coverage Levels: Opting for higher coverage limits or additional types of coverage will generally increase your premium.

4. How to Choose the Right Car Insurance Policy

Selecting the right car insurance policy involves evaluating your needs and comparing options:

- Assess Your Needs: Consider your driving habits, vehicle type, and financial situation to determine the coverage levels you require.

- Compare Quotes: Obtain quotes from multiple insurance providers to find the best rate for the coverage you need.

- Check Company Reputation: Research the reputation and customer service of insurance companies to ensure reliability.

5. The Importance of Regularly Reviewing Your Policy

Regularly reviewing your car insurance policy helps ensure it remains relevant and adequate:

- Life Changes: Update your policy if you experience significant life changes, such as moving to a new location or purchasing a new vehicle.

- Coverage Gaps: Periodically review your coverage to address any potential gaps or changes in your needs.

- Premium Adjustments: Check if you qualify for discounts or if there have been changes in premium rates.

6. Common Car Insurance Myths Debunked

Several misconceptions about car insurance can lead to misunderstandings:

- Myth: The Cheapest Policy is Always Best: The lowest premium doesn’t always provide the best coverage. Evaluate the policy’s coverage and exclusions.

- Myth: Your Credit Score Doesn’t Affect Insurance Rates: In many states, your credit score can influence your insurance premiums.

- Myth: Your Insurance Policy Covers All Costs: Understand your policy’s limits and exclusions to avoid unexpected expenses.

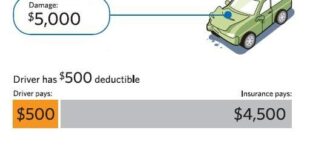

7. The Role of Deductibles in Car Insurance

Deductibles are the amount you pay out of pocket before your insurance coverage kicks in:

- Choosing a Deductible: Higher deductibles generally lead to lower premiums, but ensure you can afford the deductible amount in case of a claim.

- Impact on Premiums: Evaluate the trade-off between deductible amounts and premium costs to find the right balance.

8. Legal Consequences of Not Having Adequate Insurance

Driving without adequate insurance can result in severe legal consequences:

- Fines and Penalties: States may impose fines for failing to carry minimum insurance coverage.

- License Suspension: Your driver’s license could be suspended if you’re caught driving without proper insurance.

- Legal Liability: Without insurance, you could be held personally liable for damages and legal fees resulting from an accident.

9. Tips for Saving on Car Insurance

There are several strategies to reduce your car insurance costs:

- Bundle Policies: Combining car insurance with other types of insurance, like home insurance, can lead to discounts.

- Maintain a Good Driving Record: Avoid accidents and traffic violations to keep premiums low.

- Consider Usage-Based Insurance: Some insurers offer lower rates for drivers who don’t drive frequently.

10. The Future of Car Insurance

The car insurance industry is evolving with new trends and technologies:

- Telematics: Usage-based insurance policies that track driving habits are becoming more popular.

- Autonomous Vehicles: The rise of self-driving cars may lead to changes in insurance requirements and policies.

Tips

- Understand State Requirements: Ensure your policy meets the minimum coverage requirements for your state.

- Evaluate Coverage Options: Consider additional coverage types based on your needs and circumstances.

- Check for Discounts: Look for discounts such as safe driver discounts or multi-policy discounts.

- Review Your Policy Regularly: Update your policy as your circumstances change.

- Shop Around: Compare quotes from different insurers to find the best rate.

- Consider Your Deductible: Choose a deductible that balances affordability and premium costs.

- Verify Company Reputation: Research the insurer’s reputation and customer service.

- Understand Policy Exclusions: Know what your policy does not cover to avoid surprises.

- Keep Records: Maintain documentation of your insurance policy and any changes made.

- Seek Professional Advice: Consult with an insurance agent if you’re unsure about coverage options.

FAQs

- What is the minimum car insurance requirement in California?

- California requires liability insurance with coverage of $15,000 for bodily injury per person, $30,000 per accident, and $5,000 for property damage.

- How does my credit score affect my car insurance premium?

- In many states, a higher credit score can result in lower insurance premiums, while a lower score may increase rates.

- What is the difference between liability and comprehensive coverage?

- Liability coverage pays for damages you cause to others, while comprehensive coverage protects against non-collision incidents like theft or natural disasters.

- How can I lower my car insurance premiums?

- Consider bundling policies, maintaining a good driving record, and looking for discounts to reduce premiums.

- What should I do if I get into an accident?

- Contact your insurance company, file a claim, and ensure you have all necessary documentation of the incident.

- Is car insurance required in all states?

- Yes, every state requires drivers to have some form of car insurance, although minimum coverage requirements vary.

- Can I choose my own deductible amount?

- Yes, you can choose your deductible amount, which affects your premium costs.

- What happens if I drive without insurance?

- Driving without insurance can result in fines, license suspension, and personal liability for damages.

- Are there discounts for safe driving?

- Many insurers offer discounts for maintaining a clean driving record and demonstrating safe driving habits.

- How often should I review my car insurance policy?

- Review your policy annually or whenever you experience significant life changes or updates to your vehicle.

Conclusion

Car insurance is a vital component of responsible vehicle ownership, ensuring protection and compliance with legal requirements. Understanding the various types of coverage, state-specific requirements, and factors affecting premiums can help you make informed decisions about your insurance policy. Regularly reviewing your policy and exploring options for savings can enhance your coverage and keep costs manageable.

In summary, navigating car insurance requirements involves staying informed about state laws, evaluating your needs, and choosing a policy that offers the right balance of coverage and cost. By following these guidelines and tips, you can ensure that you meet legal requirements and protect yourself adequately on the road.